5 min read

The First Step to Decarbonizing Transportation

October 1, 2024

Share:

Table of contents

Browse the table of contents to jump straight to the part you’re looking for

Introduction: Why Internal Carbon Pricing Matters

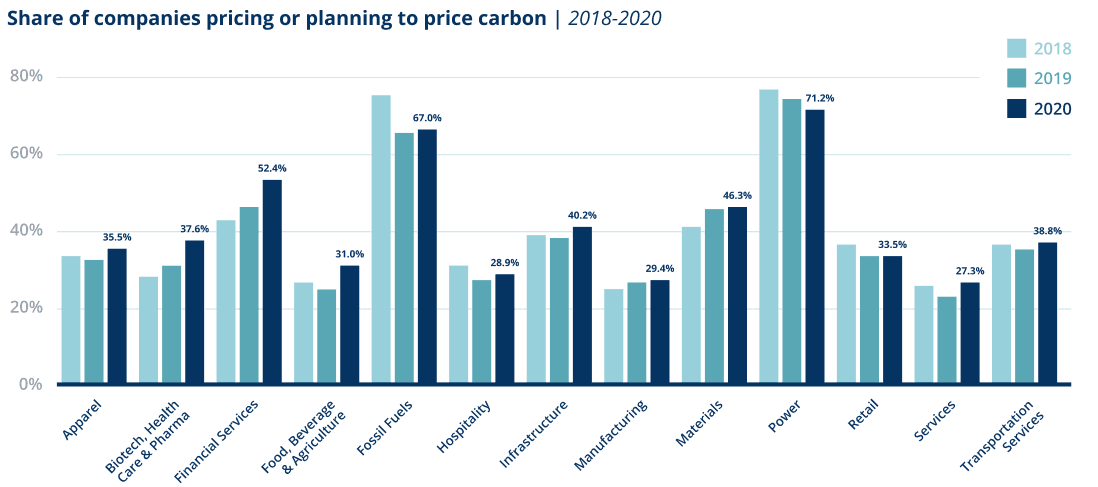

Companies are calculating the cost of carbon at increasing rates. According to the Carbon Disclosure Project (CDP), nearly half of the world’s 500 biggest companies by market capitalization reported they were putting a price on carbon or planning to within the next two years. This is an 80% increase in the number of companies planning or using an internal carbon price from 2015 to 2020. The cost of carbon can be used by governments to inform the level of carbon tax, and by companies to inform their internal carbon pricing approach. This can vary depending on the type, region, industry, and GHG emissions scope coverage.

Generally, companies’ internal carbon prices have fallen short of what is needed for alignment with the Paris Agreement. In 2020, the median internal carbon price disclosed by CDP was $25 per metric ton of CO2e. At this time, an appropriate internal carbon price would have been $40 to $80 per metric ton for alignment with the Paris Agreement. By 2030, companies should consider an internal carbon price of $50 to $100 per metric ton to reduce emissions in line with achieving the Paris Agreement.

Companies can refer to the social cost of carbon set by the government to inform their organization’s internal carbon pricing. Under the Biden administration, the federal government uses a social cost of carbon of $51, which includes impacts on a global level. The EPA has also recently proposed a much higher value of $120 to $340 per metric ton of CO2, with the corresponding price rising to $140 to $380 per metric ton by 2030.

Use an internal carbon price to drive transportation emissions reduction

- Drive investment in decarbonization initiatives across the entire transportation network

- Uncover opportunities like fuel efficiency and load fill considerations, among others

- Embrace a growth mindset to develop and adopt new processes and technologies

- Demonstrate a commitment to corporate social responsibility

Determine your internal carbon price

Calculating your internal carbon price can be an ambiguous and ambitious task. To simplify it, we broke it into three easy steps:

- Understand what you are calculating

- Find a calculation that works for you

- Calculate your internal carbon price

In the process, consider the factors that make up an internal carbon price to obtain the most value in using it for your organization.

1. Understand what you are calculating

To understand how to calculate the cost of carbon, you first need to understand what you are calculating. The main types of carbon prices used by companies are a shadow price, an implicit price, and an internal fee. A shadow price is the most common type, with half of all companies that disclosed an internal carbon price using this calculation.

- Shadow price: Calculates a hypothetical cost of carbon on each metric ton of GHG emissions. Applying a shadow price to the carbon footprint in ROI calculations improves the business case for low-carbon investments, and therefore is typically used in CAPEX decisions.

- Implicit price: Calculates the cost of emissions abatement or renewable energy procurement divided by the metric tons of emissions abated. An implicit price is used to identify the CAPEX required to meet climate-related targets and to inform a more strategic internal price.

- Internal fee: A mechanism to impose a fee on GHG emissions within your organization. Fees raised can be contributed to a low-carbon fund and used toward energy efficiency or renewable energy projects.

| Industry | Median Price USD | Max. Price USD | Unique companies with usable data |

| Apparel | $82 | $760 | $5 |

| Biotech, Health Care & Pharma | $43 | $919 | $22 |

| Financial Services | $17 | $297 | $105 |

| Food, Beverage & Agriculture | $28 | $177 | $40 |

| Fossil Fuels | $28 | $100 | $55 |

| Hospitality | $16 | $20 | $4 |

| Infrastructure | $35 | $383 | $32 |

| Manufacturing | $28 | $532 | $116 |

| Materials | $28 | $459 | $137 |

| Other Services | $20 | $146 | $78 |

| Power Generation | $23 | $112 | $77 |

| Retail | $23 | $135 | $42 |

| Transportation Services | $20 | $269 | $33 |

2. Find a calculation that works for you

Once you have the type identified, the second step includes how you are going to calculate it. An internal carbon price can be calculated based on external resources, peer benchmarking, internal consultation, and technical analyses.

- External resources: Using price projections from climate-related regulation or the social cost of carbon can be a helpful guide in calculating your cost. Energy taxes, renewable energy support tariffs, removal of fossil fuel subsidies, costs of complying with GHG emissions standards, and energy efficiency certificate trading are all available external resources.

- Peer benchmarking: Evaluate internal carbon prices set by competitors within your industry. By setting a higher internal carbon price relative to peers, you can improve your business case for developing new innovative products and services to maintain your competitive edge.

- Internal consultation: Examine past business decisions and determine the carbon price levels that would have impacted those decisions.

Technical analyses: Evaluate the required investment to achieve your company’s emissions reduction targets.

3. Calculate your internal carbon price

You have completed your research and are ready to apply it to calculate your internal carbon price! In the calculation process, include key stakeholders to capture the activities from all business units and departments, record data in an organized and actionable format, and consider how you are going to use the internal carbon price for your benefit.

Act on decarbonization initiatives with an internal carbon price

Take the first step toward meeting your emissions reduction targets by setting an internal carbon price. With the cost established for your company, you can properly budget for and act on decarbonization initiatives. Transportation, compared to some other sectors, typically encounters challenges in keeping pace with technological innovation. However, with scope 3 emissions comprising around 90% of companies’ total carbon output and transportation emissions being one of the most consistent and significant contributors across industries, the sector offers a tremendous advantage to fight climate change.

Ready to take the first step toward decarbonizing transportation?

Discover how CleanMile can help you measure, manage, and reduce emissions across your transportation network.

Download the report

Take the full The First Step to Decarbonizing Transportation: Establishing an Internal Carbon Price report with you. Download your copy to save these insights for future reference or to share them with your team.