Breakthrough's Monthly Freight Index

Breakthrough's freight index is your monthly source for U.S. freight market intelligence. Built on shipper-transacted data from Breakthrough's dataset, it gives transportation leaders an updated view of market trends, enabling you to take confident action.

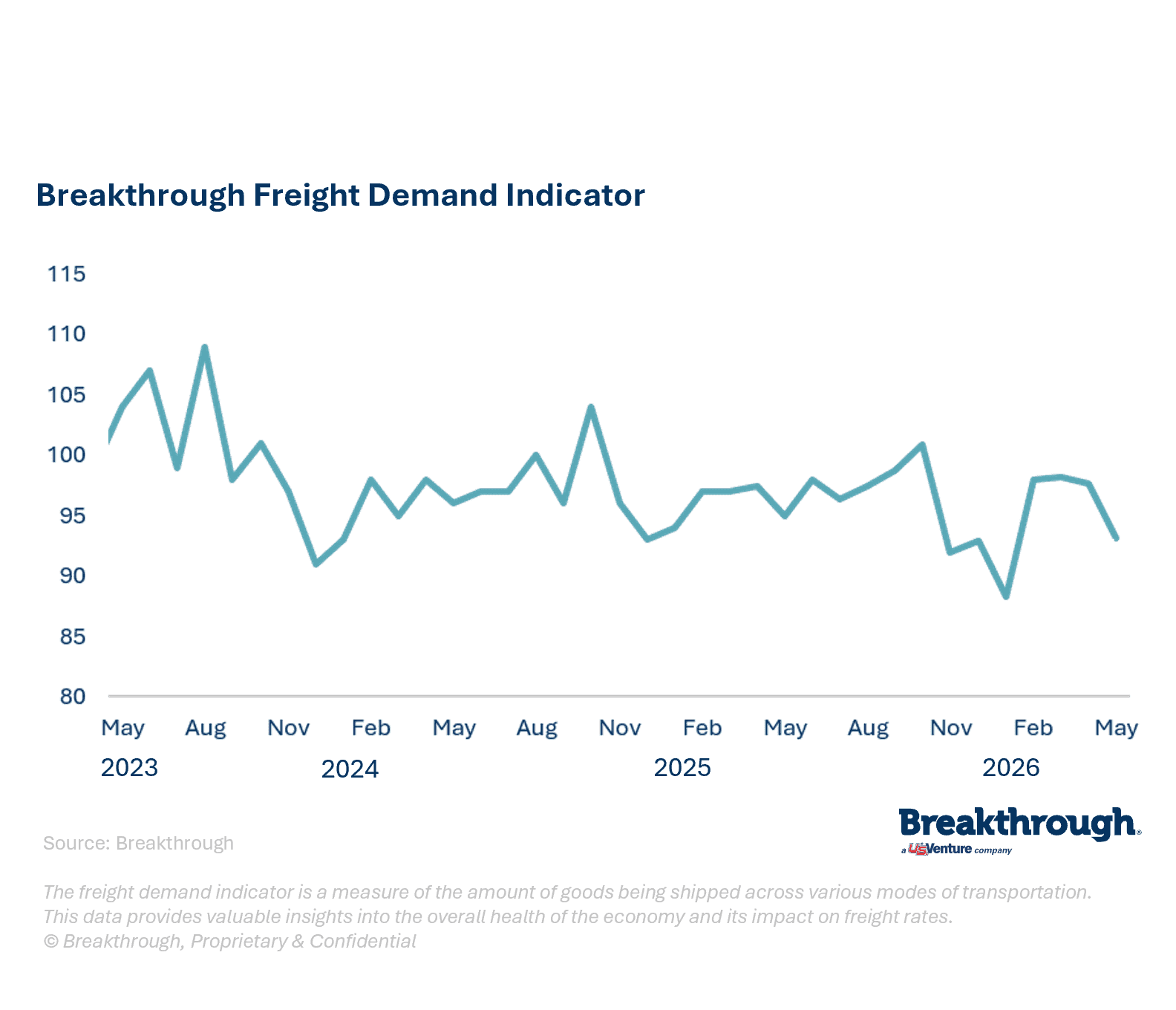

Freight index analysis

Breakthrough's freight index edged up 0.2% year-over-year in May, continuing the recent oscillating pattern. Paper and packaging led the way at 9.1%, likely reflecting front-running ahead of anticipated price increases, while retail posted a 4.7% gain supported by general merchandise and discount-oriented retailers. Durable goods fell 3.3%, consumer packaged goods declined 4.8%, and food and beverage slipped 2.6%, consistent with a consumer squeezed by elevated energy costs and persistent inflation.

A resolution of the Iran conflict, ideally at the conclusion of the short-term peace agreement, stands out as the most notable near-term variable, since energy price relief would deliver a meaningful tailwind. The Freight Demand Indicator forecast moves modestly higher to 1.7% growth, though underlying conditions remain fragile.

Freight market update

Published: July 1, 2026

Freight demand held essentially flat year-over-year in May. Breakthrough's freight volumes rose just 0.2%, as gains in paper and packaging and retail offset softness in durable goods, consumer packaged goods, and food and beverage. The macro backdrop stayed mixed, with a resilient labor market countered by inflation at 4.2%, which continues to pressure consumer spending. The Fed held rates steady in June, though increases remain possible.

Truckload capacity is the dominant rate driver, shaped by regulatory enforcement, the broker liability ruling, and rising costs. Rate forecasts moved sharply higher after CVSA Roadcheck week, with dry van seeing the largest shift.

What is affecting freight demand right now?

Freight demand reflects a mix of macroeconomic pressures and shifting market dynamics.

Each of these dynamics carries direct implications for how shippers plan, procure, and benchmark their transportation networks.

Understanding what's driving the current market and what it means for your network is the first step toward making confident, data-driven decisions in today's rapidly shifting environment.

Macroeconomic factors

Inflation at 4.2% continues to squeeze consumer spending, even as a resilient labor market provides some support.

Industry and sector dynamics

Softness in durable goods, consumer packaged goods, and food and beverage points to a consumer strained by elevated energy costs and persistent inflation.

Policy and market drivers

Regulatory enforcement, the broker liability ruling, and rising costs are shaping truckload capacity.

What this means for shippers

Ground decisions in data

Benchmark against shipper-transacted data reveals cost gaps, improvement opportunities, and stronger positioning in carrier conversations.

Evaluate your carrier mix

Review your carrier mix by lane and identifying whether alternatives exist can help protect service levels and manage costs.

Plan for a gradual recovery

Leverage unbiased, data-driven market expertise to effectively communicate market dynamics to your C-suite, enhancing your credibility as a transportation leader.

About Breakthrough's Dataset

The Breakthrough ecosystem is one of the cleanest and most robust sets of transportation data in the U.S.

46.5 million shipments

$35 billion in transportation spend

16.5 billion commercial miles

2.5 billion gallons of diesel fuel

Frequently asked questions

Stay Ahead of Freight Market Changes

The freight market doesn't stop. Shippers need to stay informed, plan ahead, and act on real-time, lane-level data.