5 min read

A Guide to the European Union's Emissions Trading System

January 1, 2025

Share:

Table of contents

Browse the table of contents to jump straight to the part you’re looking for

- Introduction

- Key Takeaways

- Understanding the Mechanics of the European Union Emissions Trading System

- The Fit for 55 Modification to the Emissions Trading System

- Emissions Trading System Allowance Price Trends

- FAQs About the European Union Emissions Trading System

- EU’s Shift Toward Battery Electric, Fuel Cells, and Hydrogen for Heavy-Duty Vehicles

Introduction

Across the globe, regulatory bodies are advocating and implementing numerous policies aimed at decarbonizing our world. In the United States, shippers are diligently tracking these developments at both the federal and state level. Concurrently, those operating within the European Union (EU), a pioneer in the realm of clean energy, are responding to strong regulations and a rising carbon price. The EU has led the way in establishing an effective carbon pricing system that spurs the private sector to embrace sustainable changes. It is of paramount importance for shippers in the U.S. to closely observe the EU’s activities, as they provide valuable insights into potential future trends in their own region.

The European Union's success in reducing emissions can be attributed in part to the widespread adoption and coverage of its cap-and-trade carbon pricing system, known as the Emissions Trading System (ETS). Participants in the EU’s Emissions Trading System include the 27 EU member states, as well as Iceland, Liechtenstein, and Norway. Currently, the ETS encompasses power generation, energy-intensive industries, and civil aviation within the European Economic Area. However, in line with the EU’s heightened ambitions to reduce emissions, the ETS is set to expand its scope in the forthcoming years, incorporating transport emissions, among others.

Key Takeaways

- The EU Emissions Trading System is a cap-and-trade model.

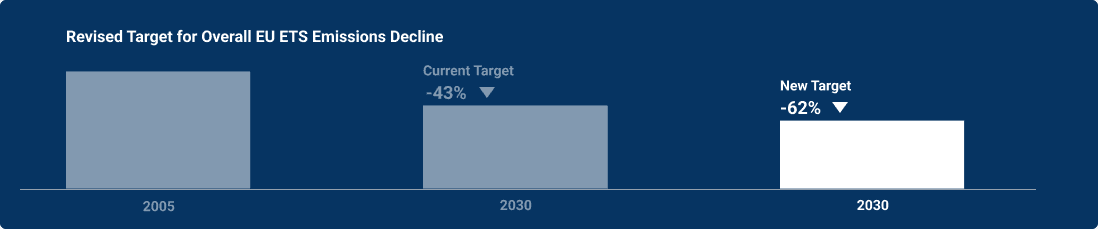

- The Fit for 55 modification changed the current ETS emissions reduction target from 43% to 62% by 2030.

- The EU intends to reduce the number of allowances within the ETS more aggressively in the coming years.

- The EU ETS II is currently slated for 2027, however, it may be postponed to 2028.

Understanding the Mechanics of the European Union Emissions Trading System

The EU Emissions Trading System is a cap-and-trade model, meaning that the EU sets a cap on the amount of CO₂ that can be emitted for a given year, with linear declines every year. In accordance with the cap volume, a certain number of allowances are made available each year, either through auction or free allocation. Each allowance represents one tonne of CO₂. Entities covered under this system must surrender the appropriate number of allowances at the end of each calendar year to offset their CO₂ emissions. They can do this either by buying allowances or curtailing emissions.

The industries and sectors subject to the cap are comprised of power generation and energy-intensive industries. These include:

- Oil refineries

- Steelworks

- Producers of iron, aluminum, cement, paper, and glass

- Civil aviation within the European Economic Area

However, it is worth noting that the scope of coverage will undergo changes in the forthcoming years.

The Fit for 55 Modification to the Emissions Trading System

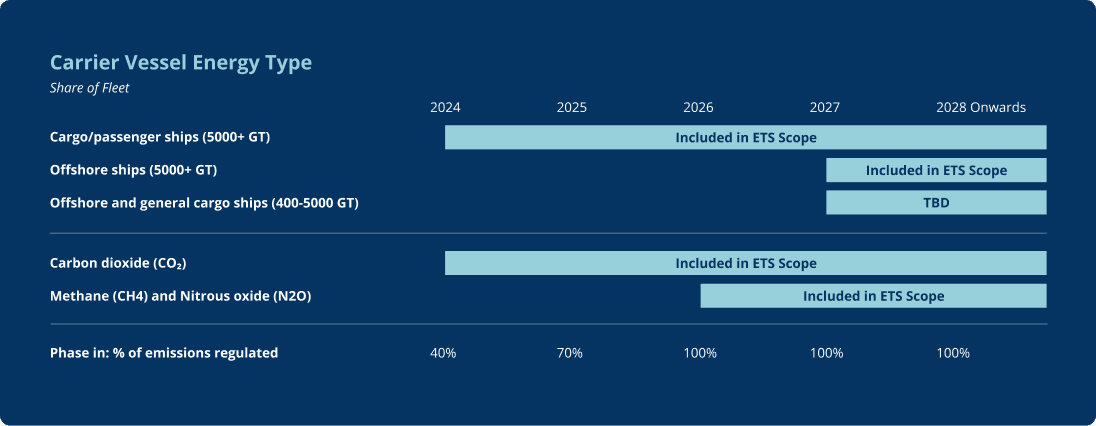

The Fit for 55 is a large legislative and regulatory package launched by the EU with the objective to reduce greenhouse gas emissions by at least 55% by 2030. This ambitious plan modified the ETS to include maritime transport and create a new system for monitoring and reporting CO₂ emissions from road transport. With this change, the current ETS emissions reduction target went from 43% to 62% by 2030, which is a 4.3% reduction per year from 2024 to 2027, and a 4.4% reduction per year from 2028 to 2030.

Emissions Trading System Allowance Price Trends

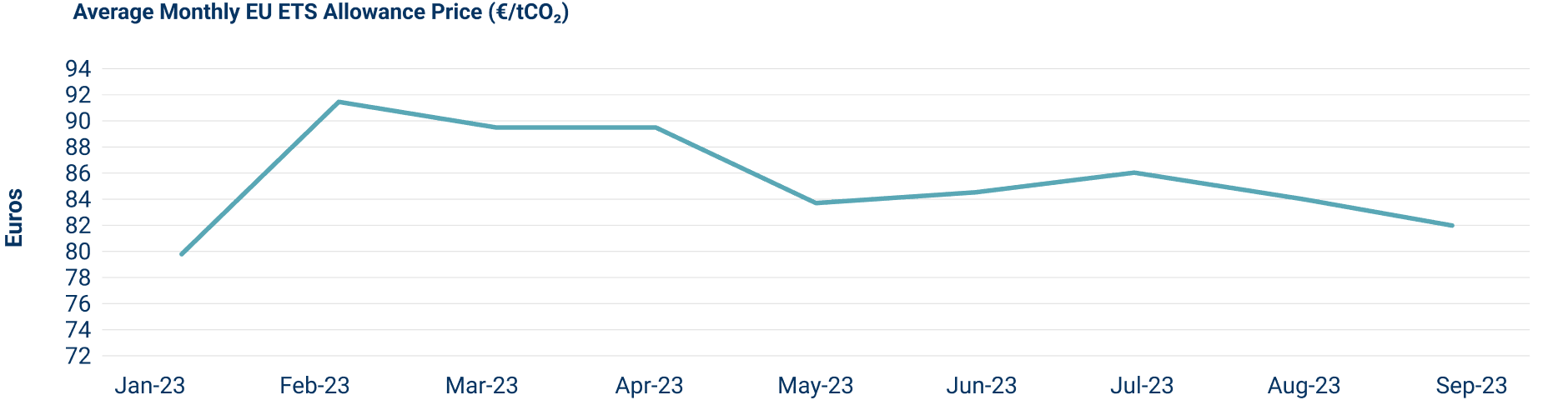

In recent years, the price of ETS allowances have seen some significant fluctuations. As per the data available in late summer 2023, the EU ETS carbon allowance price has trended around EUR 82–84, roughly USD$90. The EU intends to reduce the number of allowances within the ETS more aggressively in the coming years. This strategy is aimed at spurring more impactful actions from the industries covered in the system. The reduction in the number of allowances essentially means that companies will have fewer free permits to emit CO₂, thereby encouraging them to innovate and invest in more sustainable technologies and processes.

As the number of allowances decrease, the price is likely to increase. Many companies are already preparing for these changes. For instance, Maersk is using a price of EUR 90 in its preparations for the ETS expansion to maritime shipping. This forward-thinking approach helps ensure that they are well-prepared to manage the financial implications of the changing ETS regulations.

FAQs About the European Union Emissions Trading System

- What effect does the emissions trading system have on maritime shipping?

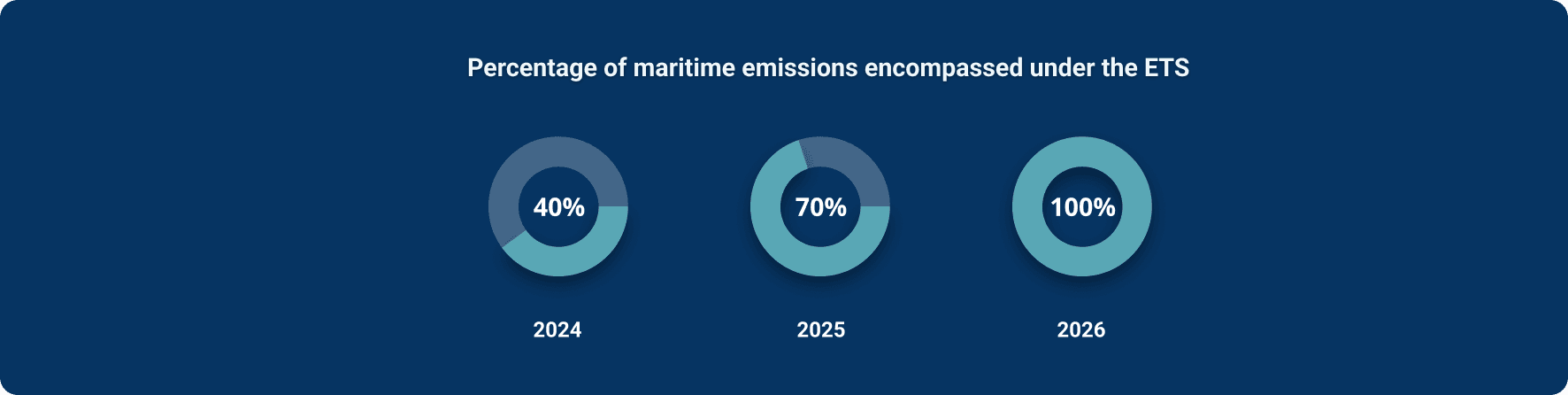

Commencing in 2024, the ETS will progressively incorporate emissions from the maritime sector based on ship size and type. Specifically, in 2024, 40% of maritime emissions will be encompassed under the ETS. This percentage will increase to 70% in 2025, and by 2026, 100% of emissions will be included. Furthermore, 100% of emissions from intra-European routes and 50% of emissions from extra-European routes to and from the EU will be covered by the ETS.

- How much will the emissions trading system cost a shipper?

In this example, a shipper is running a U.S. to Europe maritime shipping route with a large cargo ship capable of carrying over 5,000 gigatons. Under these conditions, Breakthrough would use the following parameters to determine the cost impact in 2024:

Calculate the cost impact:

1. Determine well to wake emissions in metric tons of CO2 per TEU.

2. Adjust for emissions in Scope.

Well to wake emissions in metric tons of CO2 per TEU

x 0.50 extra-European emissions factor (intra-European is 100%)

x 0.40 emissions in scope (40% in ‘24; 70% in ‘25; 100% in ‘26)

[xx] metric tons of CO2

3. Apply emissions allowance cost.

[xx] metric tons of CO2

x EUR 82.01 per metric ton CO2 (Average monthly allowance price)

Approximate EUR cost impact per TEU

- How should shippers plan for European Union’s Emissions Trading System II?

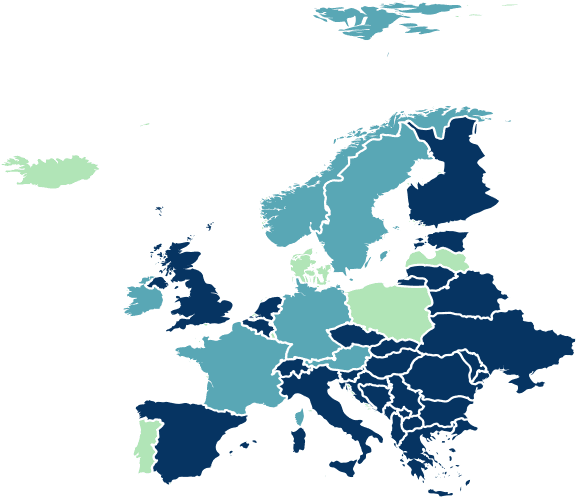

The forthcoming segment of the EU ETS, referred to as EU ETS II, signifies a strategic expansion to encompass fuel distribution and fuel suppliers for road transport, buildings, and additional industrial sectors. The EU ETS II is currently slated for 2027, however, it may be postponed to 2028 to protect citizens from high energy prices brought forth by the Russia-Ukraine war. The allowance cap on emissions for the ETS II will have a linear reduction factor of 5.15% from 2024 and 5.43% from 2028, suggesting that allowance prices under the ETS II may rise quickly over time compared to ETS. To reduce the potential ramifications of this scenario, a price stability mechanism has been considered that would release 20 million additional allowances if the price of an allowance in ETS II rises above 45 EUR. Key stakeholders are doubtful the price stability mechanism will be effective. Using an allowance cost estimate of EUR €45, the added cost per liter of diesel is EUR €0.12, or an additional cost of around USD $0.49/gallon of diesel. We can expect this cost impact to vary widely due to the many aspects at play in this new policy. For example, member states can exempt fuel suppliers until 2030 if there is a national CO₂ price that is equal to or higher than the new ETS price. In the map above, you can view countries where fuel suppliers either qualify or may qualify in the future for the exemption until 2030. |  Countries in teal have carbon prices in place on the transport sector that already reach, or are expected to increase to EUR45, which would allow that country to exempt fuel suppliers from the EU ETS II cost until 2030. Countries in green have relevant carbon prices that do not reach, or are unlikely to reach, EUR45 in the EU ETS II timeframe. Iceland, Liechtenstein, and Norway are included here because they are members of the EU ETS, although not the EU. | |

EU’s Shift Toward Battery Electric, Fuel Cells, and Hydrogen for Heavy-Duty Vehicles

The EU is prioritizing battery electric, fuel cells, and hydrogen as primary energy sources for heavy-duty vehicles. In the press release for the proposed revisions to the heavy-duty vehicle emissions standards, the European Commission suggested that the use of renewable fuels for heavy-duty vehicles, such as biodiesel and renewable diesel, could potentially divert these sources from other sectors like aviation and maritime, which have fewer clean fuel alternatives.

However, some nations, notably Germany, have been adamant about not eliminating internal combustion engine (ICE) vehicles entirely; they have instead proposed the use of e-fuels. This stance could influence how stringently the EU adheres to allocating biodiesel and renewable diesel to the maritime and aviation sectors.

Looking to navigate the complexities of Europe's evolving emissions regulations?

Discover how Breakthrough's fuel management solutions can help you optimize costs, reduce emissions, and stay compliant with EU standards.

Download the white paper

Take the full A Guide to the European Union’s Emissions Trading System white paper with you. Download your copy to save these insights for future reference or to share them with your team.